Nigeria's Debt at ₦159 Trillion: Who We Owe, When We Started, and Whether It Will Ever End

From a £5.7 million colonial loan in 1923 to ₦159 trillion today, this article breaks down Nigeria’s debt- who we owe, when repayments are due, why borrowing persists, and whether the cycle can end.

Prefer listening? Tap play and the article will be read aloud.

CO-WRITTEN WITH SEYI AJAYI

Nigeria’s debt is one of those topics everyone hears about but few fully understand. ₦159 trillion is not just a headline figure, it’s a reflection of decades of borrowing, policy decisions, economic shocks, and, at times, poor fiscal discipline. Yet for many Nigerians, the real impact of this debt is not in the numbers. It shows up in everyday life, rising costs, limited public services, and an economy that constantly feels under pressure.

This article takes a clear look at Nigeria’s debt: how it started, who the country owes, when repayments are due, and why borrowing continues. More importantly, it asks the question that matters most, is Nigeria in a debt trap, and can it realistically get out?

THE NUMBERS RIGHT NOW

Nigeria's total public debt stood at ₦159.28 trillion (approximately $110.97 billion) as of December 31, 2025, according to the most recent comprehensive figures released by the Debt Management Office (DMO) in April 2026. That is a 3.9% rise from the ₦153.29 trillion recorded at the end of September 2025, and a 10.1% increase year-on-year from ₦144.67 trillion in December 2024.

To put this in everyday terms: if Nigeria's entire debt were split equally among every citizen, from newborns to the elderly, each person would owe roughly ₦724,000. You will not receive a bill, but you are already paying. Through inflation, infrastructure gaps, rising taxes, and the slow erosion of public services that debt servicing crowds out.

Of the total debt, domestic borrowing accounts for ₦84.85 trillion (53%), while external debt stands at ₦74.43 trillion (47%). The Federal Government holds the lion's share, ₦146.76 trillion, while Nigeria's 36 states and the FCT collectively owe ₦12.52 trillion.

WHO NIGERIA KNOWS

Source: RipplesNigeria

Domestically, the government borrows primarily through FGN Bonds- securities purchased by local banks, pension funds, insurance companies, and institutional investors. FGN Bonds make up about 80% of domestic debt, with Treasury Bills accounting for roughly 17%. Nigeria's pension sector alone holds an estimated ₦14 trillion in government bonds through the Pension Commission (PenCom).

On the external side, the World Bank Group is Nigeria's single largest foreign creditor, with approximately $18.3 billion in outstanding credit, making Nigeria the third-largest debtor to the World Bank's International Development Association (IDA). The African Development Bank (AfDB) holds around $3.5 billion, while commercial Eurobond investors account for approximately 17% of external debt.

Among bilateral creditors, China's Exim Bank leads with $4.91 billion, representing over 80% of Nigeria's bilateral debt. France, Germany, and Japan also hold smaller portions

WHEN THE BILLS ARE DUE

Not all debt falls due at once. The DMO's strategy targets an average time to maturity of 11 and 13 years, meaning most obligations are spread over the long term. About 14% of Nigeria's debt is due within one year.

Debt servicing is already one of Nigeria's heaviest fiscal burdens. In 2024, the country spent approximately $8.55 billion servicing its debt - a figure that continues to grow. As of April 2026, the budget projects a deficit of over ₦23.85 trillion (about 4.28% of GDP), which means the government must keep borrowing to cover the gap between what it earns and what it spends.

In November 2025, Nigeria issued a $2.35 billion Eurobond split across 10-year and 20-year maturities, extending its debt repayment profile further into the future. On the positive side, Nigeria cleared its IMF COVID-era loan in April 2025, and its debt-to-GDP ratio is projected to fall to 32.3% in 2026, down from 35.5% in 2025.

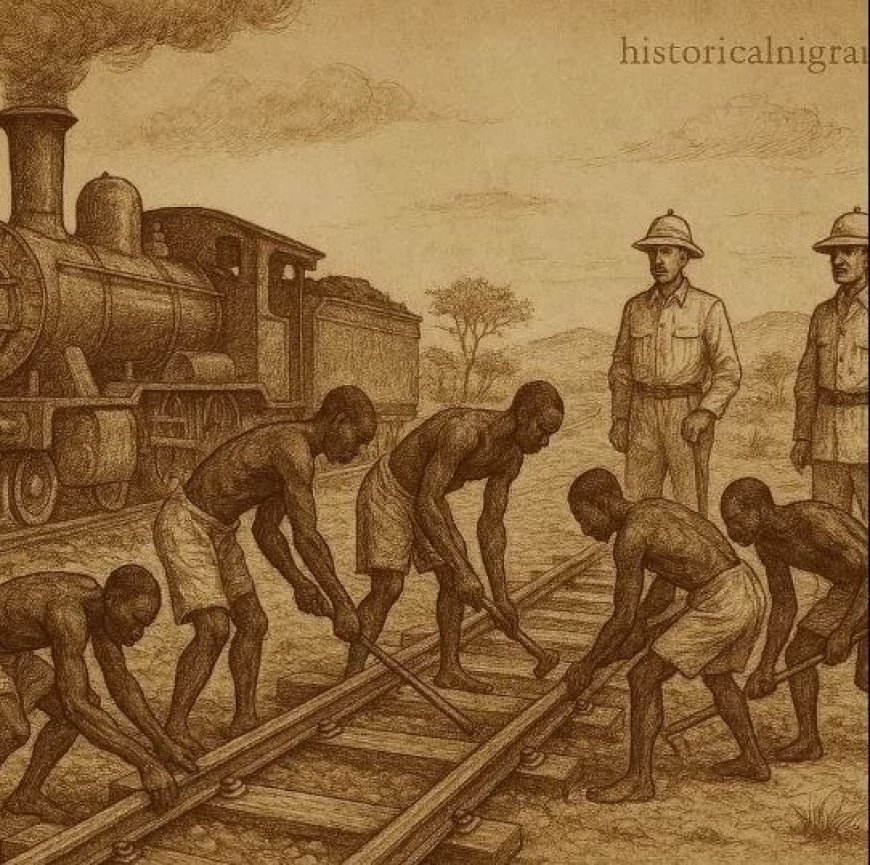

HOW IT ALL STARTED

Source: Historical Nigeria

Nigeria's borrowing did not begin with independence. In 1923-1924, the British colonial administration took out a £5.7 million loan to fund railways and ports infrastructure built to extract resources, not develop local communities. That loan was repaid over 20 years. It was just the beginning.

The 1970s oil boom brought euphoria and reckless spending in equal measure. Nigeria borrowed heavily on the assumption that oil revenue would always cover the bills. By 1980, external debt had reached $8.9 billion. Then oil prices crashed. The 1980s and 1990s were defined by the economic crisis, debt peaked at $28.7 billion in 1997 and the country fell into a cycle of rescheduling payments it could not afford.

The turning point came in 2005, when President Olusegun Obasanjo secured an $18 billion debt write-off from the Paris Club. By paying $12 billion upfront, Nigeria cleared $30 billion in total foreign debt, a deal widely regarded as the most consequential economic decision in the country's post-independence history.

The relief did not last. From ₦12 trillion in 2015, Nigeria's debt has ballooned to ₦159 trillion by the end of 2025, a thirteenfold increase in a decade. The naira's devaluation significantly inflated the naira value of foreign debt, but new borrowings also accelerated under successive administrations.

WHY NIGERIA KEEPS BORROWING

The drivers of Nigeria's debt are structural and recurring. Oil price volatility remains the central problem: a country that depends on a single commodity for the majority of its revenue has no stable fiscal footing. When prices fall, deficits widen and borrowing fills the gap.

Decades of fuel subsidy spending drained billions that could have funded infrastructure or reduced the need for borrowing. Currency devaluation - particularly the sharp depreciation of the naira, mechanically inflates the naira value of dollar-denominated debt without a single new loan being signed.

Infrastructure needs have also driven borrowing, particularly from China. The Abuja-Kaduna and Lagos-Ibadan rail lines, for instance, were financed largely through Chinese Exim Bank loans. COVID-19 added another layer: the government borrowed from the Central Bank through Ways and Means Advances and from international institutions to manage the economic shock.

Underneath all of this is a revenue problem. Nigeria consistently collects far less tax relative to its economy than comparable countries. Until that changes, borrowing remains the default answer to every funding shortfall.

WILL THE DEBT TRAP EVER END?

Source:Tekedia

The honest answer, not easily and not soon. Nigeria's debt-to-GDP ratio of 32.3% is not unusually high by global standards, many economies carry far heavier loads. The more pressing concern is debt servicing as a share of revenue. When a government spends more paying interest than it invests in health, education, or infrastructure, debt stops being a tool for development and becomes a drain on it.

The DMO's Director-General, Patience Oniha, speaking at the 2026 IMF Spring Meetings in Washington in April, stressed that every loan requires National Assembly approval before it can be contracted, a reminder that borrowing is governed by process, even if the outcomes have sometimes been poorly managed.

Structural reform, broadening the tax base, reducing oil dependence and plugging revenue leakages is the only durable path out. Borrowing to invest in productive assets can be rational; borrowing to pay salaries and service old debt is a spiral.

For ordinary Nigerians, the debt is already being paid, not through a bill in the post, but through petrol prices, school fees, crumbling hospitals, and a currency that buys less every year. Whether the government uses borrowed money wisely enough to reverse that reality remains, as it has for decades, the defining question.

CONCLUSION

Nigeria’s debt story is not just about how much is owed, It is about what that borrowing has achieved, and what it continues to cost.

The country is not yet at a point of collapse, but the warning signs are clear. When debt servicing consumes a large share of government revenue, it limits investment in the very sectors that could drive growth and reduce the need for future borrowing.

Ending the cycle will require more than optimism or short-term fixes. It demands consistent fiscal discipline, stronger revenue generation, and a clear shift toward borrowing that actually produces measurable economic value.

Until then, the burden of Nigeria’s debt will continue to show up where it matters most, not in government reports, but in the daily realities of its people.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0